April is Financial Literacy Month, making it the perfect time to focus how we understand and manage money.

Financial literacy is more than knowing what money is, it’s having the skills and confidence to make smart financial decisions every day. It’s how we spend, save, borrow, and plan for the future.

And, here’s the important part: financial literacy isn’t something you learn once. It’s something you build over time and it’s never too early to start!

Why Financial Literacy Matters at Every Age

Everyone has a financial life. Whether you’re managing your first allowance or planning for retirement, the way you handle your money shapes your future.

Financial literacy increases the likelihood of achieving financial well-being, a state where you can meet your current obligations, feel secure about the future, and make choices that allow you to enjoy life. [1]

Strong financial knowledge helps people:

- Stay on top of everyday expenses

- Prepare for unexpected costs

- Make choices that improve their quality of life

- Build toward financial well-being

That’s why starting early matters. The habits we learn as kids often carry into adulthood.

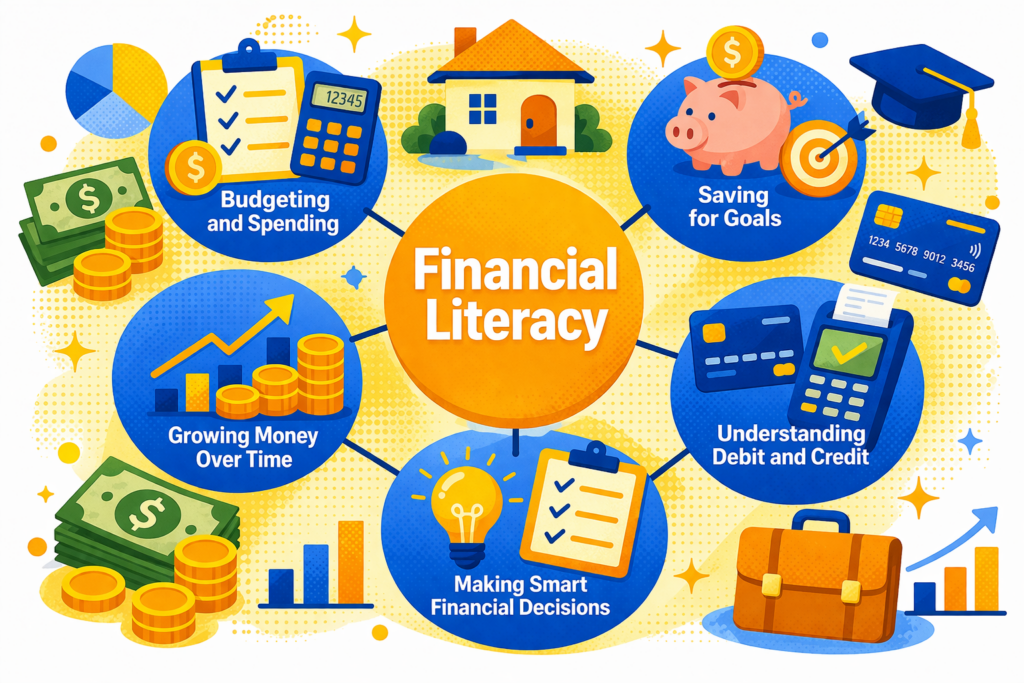

The Core Skills of Financial Literacy

Financial literacy is built on a few key skills and each one can be introduced in simple, age-appropriate ways. Let’s talk about each core skill!

1. Budgeting and Spending

Budgeting is all about understanding your choices and making a plan for how your money works for you.

For kids, that might look like:

- Deciding how to spend birthday or allowance money

- Learning the difference between needs and wants

- Setting aside a portion of money for saving before spending

For adults, budgeting becomes more structured and has more consequences. Financial experts recommend starting with a simple plan:

Know your numbers

Track your total monthly income and all expenses. This includes fixed costs like rent or a mortgage, as well as variable expenses like groceries, gas, and entertainment.

Separate needs from wants

Prioritize essentials such as housing, utilities, food, transportation, and insurance before spending on non-essential items.

Create a spending plan

A common guideline is the 50/30/20 approach:

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

This framework helps ensure your essentials are covered while still making progress toward your goals. Explore this 50/30/20 calculator below!

Track and adjust regularly

Budgets are not static. Reviewing your spending each month helps you identify patterns, adjust where needed, and stay on track.

Plan for irregular expenses

Set aside money for things like car repairs, holidays, or annual bills so they do not disrupt your monthly budget.

According to the Consumer Financial Protection Bureau, creating and maintaining a budget is one of the most effective ways to stay in control of day-to-day finances and avoid unnecessary debt. [1]

Check out our blog post on making a budget you can actually stick to!

2. Saving for Goals

Saving is how you turn plans into reality and protect yourself from the unexpected.

For kids, saving might start with:

- Setting aside money for a toy or game

- Learning patience by working toward a goal

- Using jars or envelopes to divide money into “spend,” “save,” and “share”

- Explore a dedicated Youth Savings Account. Our Sun East Youth Savings Accounts have no monthly fees and a low $5 opening deposit!

For Adults, Build an Emergency Fund First

Experts recommend setting aside enough to cover 3–6 months of essential expenses. This provides a cushion for unexpected events like job loss, medical bills, or car repairs. [1]

Set Clear Savings Goals

Break goals into categories:

- Short-term: vacations, holidays, purchases

- Medium-term: car, education

- Long-term: homeownership, retirement

Automate Your Savings

Set up automatic transfers so saving happens consistently without needing to think about it. Check out our digital banking services to explore the features available to you!

Start Small and Stay Consistent

Even small amounts add up over time. Consistency matters more than starting big.

According to the Consumer Financial Protection Bureau, having savings improves financial stability and helps individuals handle unexpected expenses without relying on debt. [1]

3. Understanding Credit and Debt

Understanding how money moves in and out of your accounts is a critical part of financial literacy.

For younger learners, this starts with:

- Knowing that debit uses money you already have

- Recognizing that credit means borrowing money that must be repaid

As you gain experience, this becomes more nuanced.

Know the Difference

- Debit cards pull directly from your checking account

- Credit cards allow you to borrow money up to a limit and repay it later

Use Credit Responsibly and Understand the Cost of Borrowing

- Pay your balance on time, every time

- Avoid carrying high balances

- Keep your credit utilization below 30% of your limit

- Interest and fees can add up quickly, so pay attention to the terms

Want to learn more about credit? Check out our blog post on Credit and how it can help you reach your financial goals.

Monitor Your Credit

Check your credit report regularly and understand how your behavior affects your credit score. AnnualCreditReport.com, the official site authorized by federal law, encourages people to review their credit history regularly and explains that credit reports play an important role in financial life. Check out this blog post to learn more about what goes into your credit score.

The Federal Deposit Insurance Corporation emphasizes that responsible credit use is key to building a strong financial foundation and accessing better financial opportunities in the future. [2]

4. Growing Money Over Time

Saving is important, but growing your money is how you build long-term financial security. For beginners, this starts with understanding that money can earn more money over time.

Take Advantage of Compound Growth

The earlier you start saving or investing, the more time your money has to grow.

Use the Right Tools for Your Goals

- Savings products for short-term needs

- Retirement accounts and investments for long-term growth

Check out this blog post to learn abouts savings products that can help you resist inflation.

Be Consistent Over Time

Regular contributions, even small ones, can lead to significant growth.

Understand Risk and Return

Higher potential returns often come with higher risk. Choose options that align with your comfort level and timeline.

According to the U.S. Department of the Treasury, saving and investing are essential steps toward building wealth and preparing for future financial needs. [3]

5. Making Smart Financial Decisions

Financial literacy is not just about knowing what to do, it’s about making informed decisions in real-life situations.

For kids, this may look like:

- Comparing two items before buying

- Deciding whether to spend now or save for later

For adults, decision-making becomes more complex, but the same principles apply.

Compare your Options

Whether choosing a loan, credit card, or savings account, take time to review terms, rates, and fees.

Think Long-Term

Consider how today’s decisions will impact your future finances.

Avoid Impulse Decisions

Give yourself time before making major purchases or financial commitments.

Ask Questions and Seek Guidance

You do not have to navigate financial decisions alone. Trusted financial institutions can help you understand your options. Visit your local Sun East Branch or contact us anytime with your questions! Also, you can check out our blog for more personal finance articles!

The Consumer Financial Protection Bureau highlights that informed financial decision-making is a key component of long-term financial well-being. [1]

Simple Ways to Build Financial Skills as a Family

Financial Literacy Month is a great time to start building healthy habits together. Here are a few easy ways to begin:

- Talk openly about money in everyday situations

- Encourage saving for short-term goals

- Give children opportunities to make small financial decisions

- Set a family savings goal and track progress together

- Lead by example with your own financial habits

Even small moments can turn into meaningful lessons.

Build Lifelong Confidence With Money

Financial literacy is not about being perfect with money. It’s about feeling confident in the decisions you make and helping the next generation feel the same.

Start small. Stay consistent. Keep learning.

Because the habits built today can shape a stronger financial future for years to come!

Sources

- [1] Consumer Financial Protection Bureau, Financial Well-Being: The Goal of Financial Education (2015). https://files.consumerfinance.gov/f/201501_cfpb_report_financial-well-being.pdf

- [2] Consumer Financial Protection Bureau, Understand Your Credit Score.

https://www.consumerfinance.gov/consumer-tools/credit-reports-and-scores/understand-your-credit-score/ - [3] U.S. Department of the Treasury, MyMoney Five. https://www.mymoney.gov/mymoneyfive

*The $10.00 contributions from Sun East are secured funds and are not available to withdraw during the promotional period of the program. The Sun East contribution will not be deposited if a monthly deposit minimum of $30.00 is not made by the participant. Any Sun East deposits added to the account will be voided should the account be closed within the promotional period of the program. This offer is available to members who open a Youth Savings Account with a monthly deposit of at least $30.00 each month for 12 months. Promotional payouts will be given after all terms of this offer have been satisfied. This offer is not valid in conjunction with any other promotional offers. Call 877-5-SUNEAST for details. #Not Transferrable.