Vacations are meant to help you relax, recharge, and make memories, but travel costs can add up quickly when you don’t have a plan. From airfare and hotels to meals, activities, baggage fees, and last-minute extras, even a simple trip can cost more than expected.

The good news? A vacation budget can help you enjoy your time away while keeping your finances on track. According to Consumer.gov, a budget helps you see how much money you have coming in, where your money is going, and where you may be able to save.

Here are a few practical vacation budgeting tips to help you plan your getaway with more confidence.

1. Add Up the Full Cost of the Trip

Before you book anything, start by estimating the full cost of your vacation. Do not stop with the hotel rate or airfare. A realistic travel budget should include everything you expect to spend before, during, and after the trip.

Common vacation expenses may include:

- Flights, gas, tolls, parking, or rental car costs

- Hotel, resort, or vacation rental charges

- Meals, snacks, coffee, and groceries

- Activities, tickets, tours, and excursions

- Baggage fees, seat selection, travel insurance, and other optional travel costs

- Pet boarding, house sitting, or airport transportation

- Souvenirs and spending money

- A cushion for unexpected expenses

This step matters because the lowest advertised price is not always the full price. The U.S. Department of Transportation notes that optional airline services can include baggage fees, advance seat selection, onboard meals, Wi-Fi, pet travel, travel insurance, and more. The DOT has also warned that surprise fees can add significant costs to what may first look like a less expensive ticket.

Check out our Vacation Affordability Calculator to help you figure out what you can afford:

2. Build Your Trip Around What You Can Comfortably Afford

Once you have a rough estimate, compare it to your monthly budget. A vacation should not make it harder to cover your regular bills, loan payments, groceries, savings goals, or other financial responsibilities.

A helpful approach is to choose your total vacation budget first, then plan the trip around that number. This helps you decide where to spend and where to scale back.

For example, you may decide to:

- Stay closer to home but spend more on activities

- Choose a less expensive hotel so you can enjoy more meals out

- Travel for fewer days but make each day feel special

- Pick one major splurge and keep the rest of the trip simple

The goal is not to take away the fun. The goal is to spend intentionally on the parts of the trip that matter most to you.

3. Start a Dedicated Vacation Fund

One of the simplest ways to prepare for a trip is to save for it separately. A dedicated vacation fund can help you track your progress and avoid mixing travel money with everyday spending. Sun East provides Vacation Club accounts that make it easy to save for travel and getaways.

MyCreditUnion.gov encourages consumers to set up automatic withdrawals to help keep up with savings goals and “pay yourself first.” You can use that same idea for vacation planning by setting aside a fixed amount each payday.

Here is a simple way to calculate your savings goal: Estimated vacation cost ÷ number of months until your trip = monthly savings target

For example, if your trip is expected to cost $1,800 and you have 6 months to save, you would need to save $300 per month. If you are paid twice a month, that equals $150 per paycheck.

Even small automatic transfers can make a difference over time. The earlier you start, the less pressure you may feel as your travel dates get closer.

If you want to explore how to create and stick to a budget, check out this blog post on creating a budget you can actually stick to!

4. Keep Emergency Savings Separate

A vacation fund and an emergency fund should have two different jobs. Your vacation fund is for planned travel. Your emergency fund is for unexpected expenses.

The Consumer Financial Protection Bureau defines an emergency fund as money set aside for unplanned expenses or financial emergencies, such as car repairs, home repairs, medical bills, or loss of income.

Try not to drain your emergency savings to pay for a trip. If a vacation would leave you without money for unexpected expenses, it may be worth adjusting the trip, choosing a lower-cost option, or giving yourself more time to save.

5. Look for Ways to Save Without Losing the Fun

Budgeting for a vacation doesn’t mean cutting out everything enjoyable. It means making thoughtful choices so your money goes further.

Consider these ways to reduce travel costs:

- Travel during off-peak times when possible

- Compare nearby airports before booking flights

- Look at road trip options if flights are expensive

- Pack light to reduce baggage fees

- Book lodging with a kitchen or kitchenette

- Plan a mix of paid activities and free local attractions

- Search for parks, beaches, museums, festivals, and community events

- Bring snacks, refillable water bottles, and travel essentials from home

- Set one planned splurge instead of making several impulse purchases

Also be cautious with deals that seem too good to be true. The Federal Trade Commission warns that some free or low-cost travel offers may come with hidden fees or may even be scams. Before paying for a travel package, rental, or deal, research the company, read the terms, and make sure you know what is included.

6. Set a Daily Spending Limit

Once transportation and lodging are covered, it is easy to lose track of everyday vacation spending. Meals, snacks, tips, rideshares, souvenirs, and small upgrades can add up fast.

To stay on track, divide your remaining spending money by the number of days you will be away.

For example: $600 spending money ÷ 5 vacation days = $120 per day

That daily limit can help guide your choices. If you spend more one day, you can balance it out with a lower-cost activity the next day.

You can also make the limit easier to follow by checking your account daily, using a notes app to track purchases, or setting aside separate amounts for meals, activities, and extras.

7. Be Careful with Credit Card Spending

Credit cards can be convenient for travel, especially for reservations, rental cars, and fraud protection. Rewards points or cash back may also help offset some costs.

But rewards only help if you avoid carrying a balance that leads to interest charges. Before using a credit card for vacation expenses, make sure you have a repayment plan. If you know you will not be able to pay the balance in full, compare your options carefully.

The CFPB explains that APR measures the interest rate plus certain fees charged with a loan, making it one of the key ways to understand the cost of borrowing. Whether you are comparing a credit card, personal loan, or another option, look at the APR, monthly payment, repayment timeline, and total cost.

If you are struggling with credit card debt, check out our blog post on strategies to get debt free.

8. Consider Whether a Vacation Loan Fits Your Budget Better

Saving ahead is usually the best way to pay for a vacation, but sometimes your travel timeline and savings timeline do not match perfectly. If you are planning a trip and want to avoid putting the full cost on a high-interest credit card, a Sun East Vacation Loan may be worth considering.

A vacation loan can give you a set loan amount, predictable monthly payments, and a clear repayment plan. That can make it easier to understand how the trip fits into your budget after you return.

Before borrowing, ask yourself:

- Will this help me avoid carrying higher-interest credit card debt?

- How much do I truly need to borrow?

- What will my monthly payment be?

- Does the payment fit comfortably into my budget?

- What is the APR this second?

- How long will repayment take?

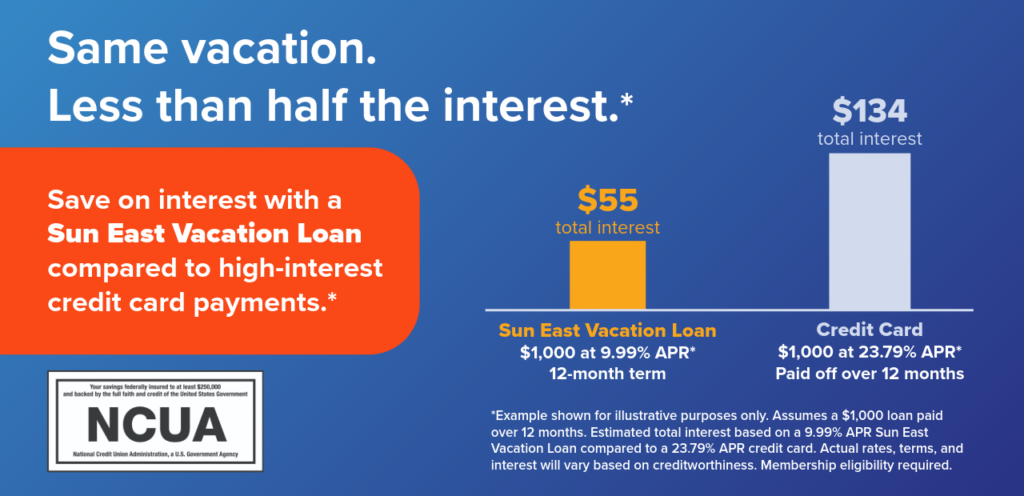

If you’re deciding how to pay for vacation expenses, the interest rate can make a real difference. Even when both options are paid off over the same 12-month period, a high-interest credit card can cost significantly more in interest than a lower-rate personal loan.

Here’s how a $1,000 vacation expense could compare:

A vacation loan should support your plans, not stretch your finances too thin. Borrow only what you need and make sure the payment works with your regular expenses.

Ready to keep your vacation plans within reach? Explore Sun East Vacation Loans and see how they can help you plan your next getaway with confidence.

Final Thoughts

A great vacation does not have to come with financial stress. By estimating the full cost, saving ahead, protecting your emergency fund, watching for hidden fees, and choosing a payment strategy that fits your budget, you can focus more on the memories and less on the money.

Whether you are planning a weekend road trip, a beach getaway, or a long-awaited family vacation, a little preparation can help you enjoy the journey from start to finish.

Sources

- Consumer.gov: Making a Budget

- U.S. Department of Transportation: Buying a Ticket

- U.S. Department of Transportation: Enhancing Transparency of Airline Ancillary Service Fees

- MyCreditUnion.gov: Savings Accounts

- Consumer Financial Protection Bureau: An Essential Guide to Building an Emergency Fund

- Federal Trade Commission: Avoid Scams When You Travel

- Consumer Financial Protection Bureau: What is the Difference Between a Loan Interest Rate and the APR?

¹APR as low as APR = Annual Percentage Rate; effective 5/18/26 and subject to change without notice. APR includes 0.25% discount for Automatic Payment Transfer from Sun East checking. Loan amounts range between $1,000 and $20,000 with term lengths ranging from 12 to 35 months. Vacation Loans will be available from May 18, 2026 to August 31, 2026. Loan rates are determined by member’s creditworthiness as well as other factors including term of the loan, line requested and loan-to-value ratio. Top tier rates listed are available to highly credit-qualified individuals. Membership eligibility required. Loans are subject to credit approval. Other conditions/restrictions may apply, call 1-877-5-SUNEAST for details.