Let’s kick off Credit Education Month with the basics! We’ll discover what credit is and how to use it to your financial advantage! We know that borrowing money makes it possible to afford things that we couldn’t otherwise, but you must understand what you’re signing up for to avoid falling into overwhelming debt!

Let’s dig in!

Paying it Back

It’s important to be clear right from the beginning: when you pay for something with credit, you’re still on the hook for that money. Often, you’ll have to pay back even more because of interest. The type of credit you use and the specifics of the agreement will determine how much interest you’ll have to pay, as well as the size and frequency of your payments.

It’s extremely important to recognize that credit can be dangerous. If you borrow too much or at too high of an interest rate, you can end up owing more than something is worth or being in a position where you’re struggling to pay back everything you borrowed.

3 Types of Credit

There are three types of credit that you’ll interact with most often:

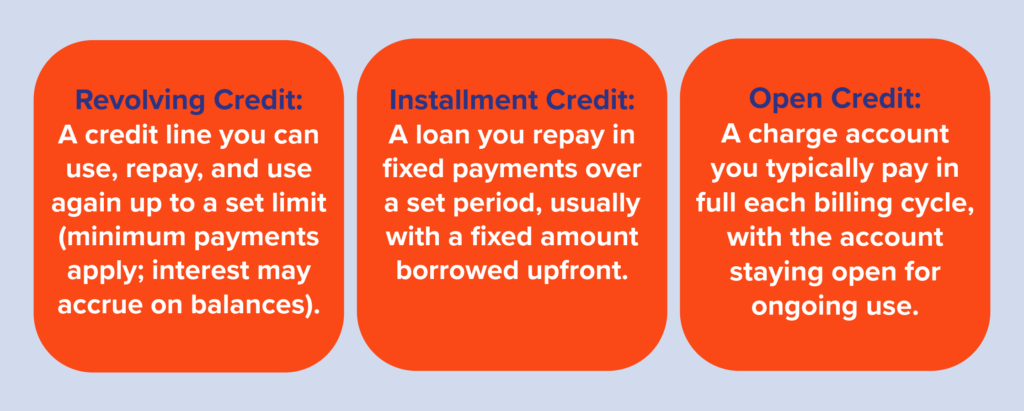

Revolving Credit

Revolving credit is a type of credit where you can borrow, pay off, and borrow again up to a predefined amount of money. At regular intervals (usually a month), you’ll need to pay back at least a minimum amount. If you don’t pay off what you borrowed completely by that time, the unpaid amount will carry over to the next billing cycle and begin accruing interest. The most common examples of revolving credit are credit cards, HELOCs, and other lines of credit.

Installment Credit

Installment credit is a type of credit where you borrow an amount of money all at once and pay it back in predetermined chunks or installments. These regular payments could last for only a few months or multiple years. Almost all loans are examples of installment credit, so that would include car loans, mortgages, and student loans.

Open Credit

The final type of credit, and one that you may not even think of as credit, is open credit. This is when you use something and then pay for it afterward in regular intervals. The most common examples of open credit are bills, like for your cell phone or utilities. You use the service on credit and then pay for what you used on your next bill. These types of bills don’t usually charge interest but will add fees if the amount isn’t paid on time or in full.

Rules for Using Credit

These rules can help keep you out of trouble and help you reach your financial goals safely:

- Rule 1: Always pay off your credit card in full so that you avoid paying interest.

- Rule 2: Pay more than your minimum on loan payments so that you pay it off faster and pay less in interest (but be aware, some loans have early payoff penalties).

- Rule 3: Keep your debt to income ratio (DTI) below 28%. To find your current DTI, add up how much you pay each month in debt payments and divide it by your gross monthly income.

- Rule 4: Don’t borrow too much at once. It’s best to keep your credit utilization ratio, or the ratio of how much you borrow versus how much you’re approved for, under 30%. So, if your credit card has a $10,000 limit, it’s best to never borrow more than $3,000 at once.

- Rule 5: Try to pay at least 20% down when buying large items like a house or car. The higher the down payment, the more you own of the item. This means you won’t have to borrow as much and you’re less likely to end up owing more than it’s worth if the market changes drastically. Figure out how much your mortgage will cost you by using our mortgage calculator.

Common Credit Terms

To be an informed credit user, you’ll need to understand these vocab terms.

A fee charged every year for using certain credit cards.

A number between 300 and 850 meant to show lenders how trustworthy you are. Your credit score is created based on your credit history, or how well you’ve used credit in the past.

An amount of money you pay upfront when taking out a loan for a large item like a house or car. Your down payment will go toward the cost of the item and lower the amount of money you have to borrow.

The amount of time you have to pay off what you’ve borrowed before interest starts to accrue. This usually only applies to revolving credit. If you pay it all off before the next billing cycle, you won’t owe interest.

The lowest amount you can pay back by a certain date in order to avoid fees.

The length of time you have to pay back the money borrowed and interest accrued on a loan.

The total amount you can borrow at one time when using revolving credit.

When you don’t pay what’s owed on a debt. This can cause a few things to happen including acceleration, where the whole debt is due immediately, damage to your credit score, and your debt being sent to collections.

A fee charged for the use of credit. Most often this fee is a percentage of the amount borrowed. One of the most common types of finance charges is interest.

A percentage of the borrowed money that must be paid back to the lender on top of what was borrowed. The interest rate can be fixed, meaning it stays the same, or variable, meaning it changes with that market.

The amount initially borrowed for a loan.

How you use credit will have a big impact on your life. Good credit—where you use credit wisely and follow the steps above—can allow you to buy things you couldn’t get otherwise. Bad credit—where you spend more than you can afford to pay back—will affect your ability to borrow in the future. Learn more about building good credit here.

This article has been republished and edited with permission. View the original article: Using Credit.