Inflation can feel sneaky. Your paycheck may stay the same, but the cost of groceries, gas, and everyday services can drift higher over time. Inflation is a general upward movement of prices, and it reduces purchasing power. In plain terms, a dollar buys less as prices rise. [1], [3]

This matters for savers because the goal is not only to grow your account balance. You also want your money to maintain its buying power over time.

How inflation eats away at spending power

The Bureau of Labor Statistics (BLS) tracks inflation through the Consumer Price Index (CPI). When CPI rises, the purchasing power of the dollar decreases. [2]

Here is the key takeaway for your savings plan:

If prices rise faster than your savings earn interest, your money can lose buying power even if your balance goes up. [4]

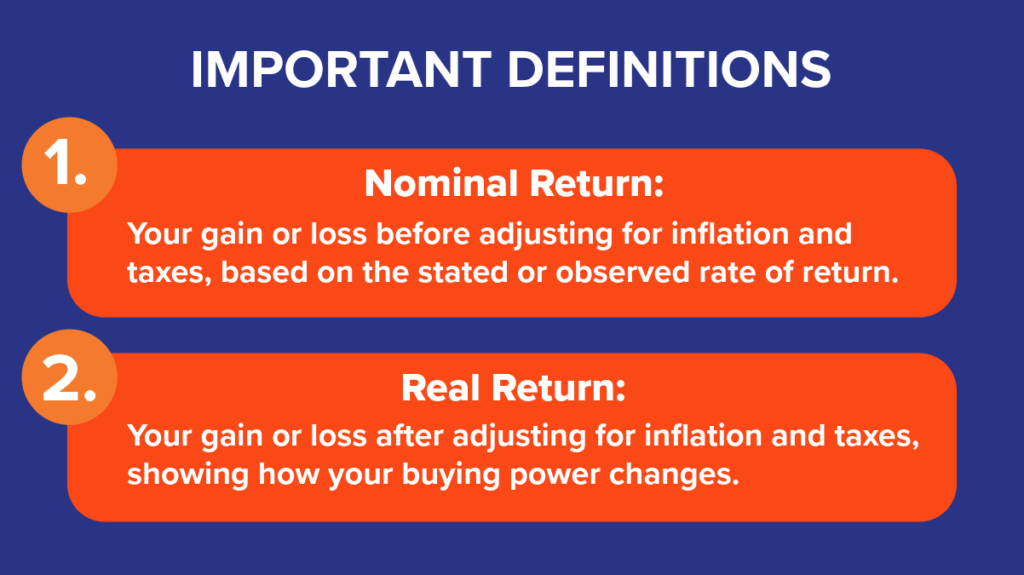

Two helpful concepts here are nominal return and real return. Use real return when considering inflation’s effect on your purchasing power. Real return is your return after you account for inflation (and, in some definitions, taxes). [5]

Why a traditional savings account may not keep up

Traditional savings accounts can play an important role, especially for short-term needs and emergency funds. The challenge shows up when the interest rate on that account stays well below inflation.

Savings Account vs Inflation

Let’s say you keep $10,000 in a traditional savings account that earns 0.50% interest for the year, compounded and credited monthly. That leaves you with a balance of $10,050.11 at the end of the year.

Now assume inflation runs at 3% over the same year. To keep up with inflation, your balance would need to be $10,300 at the end of the year.

- Shortfall in purchasing power: $10,050.11 − $10,300 = -$249.89

So even though your balance rises to about $10,050.11, you would need $10,300 to keep up with inflation. That means you effectively lost about $249.89 in purchasing power by the end of the year.

This does not mean a regular savings account is “bad.” It means you should match the tool to the job.

Options that can help resist inflation

Let’s explore some financial products that can help you fight inflation.

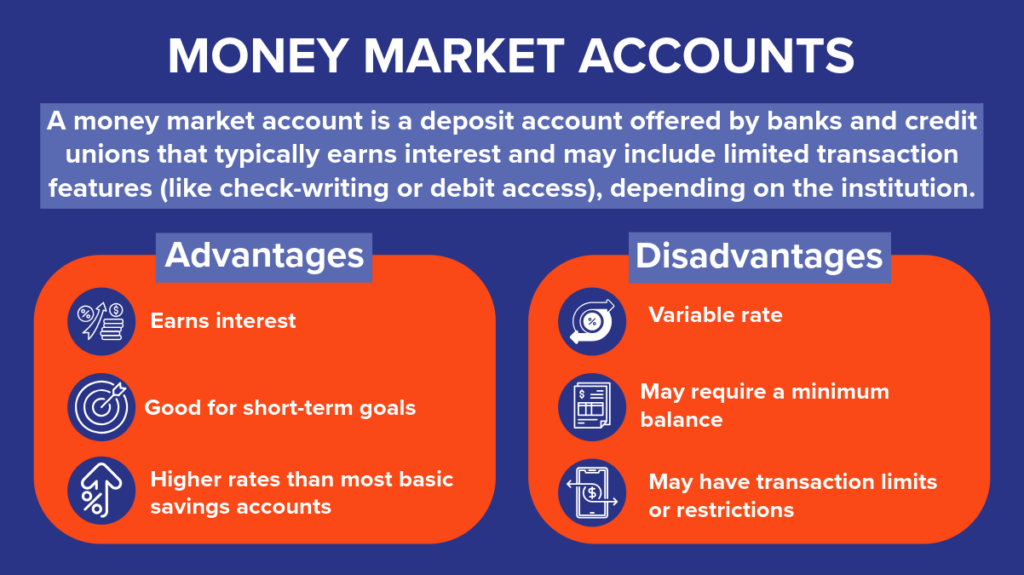

Money Market Accounts

Why People Use Money Market Accounts

- Useful for short-term savings you may need to access

- Helpful for planned, larger expenses (taxes, tuition, home projects), especially when you want to keep the money separate [8]

Money Market Account at 3.20% APY+ vs Inflation

Let’s say you keep $10,000 in a money market account that earns 3.20% APY+ for the year, considering compounded daily interest added to your balance monthly. Your balance at the end of the year would be $10,320.

Like before, let’s assume inflation runs at 3% over the year. So, you’d need a balance of $10,300 to keep up with inflation.

- Change in purchasing power: $10,320 − $10,300 = $20

In this scenario, your balance grows to $10,320, and you end up about $20 ahead of inflation in purchasing power at the end of the year.

GROW Your Savings With a Sun East GROW Money Market Account

Our GROW Money Market Account let’s you earn at 3.20% APY+ at the time of publication. This gives you a buffer against the forces of inflation, while also giving you access to your funds when you need them.

- Earn 3.20% APY+

- Access your cash anytime without penalty

- Opening deposit of $2,500 (new money)

- No maximum deposit

Learn more about how to open a GROW Money Market Account.

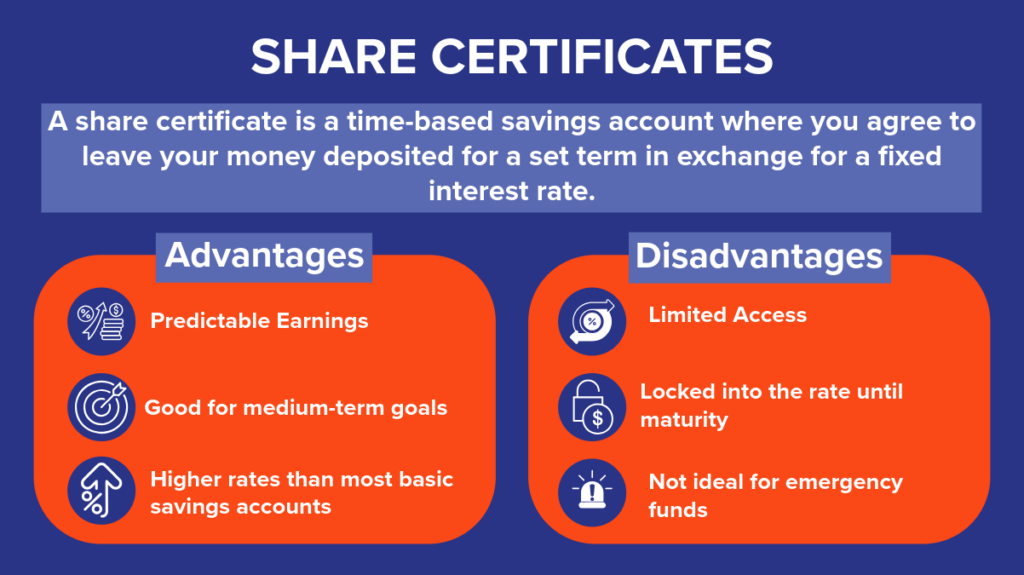

Share Certificates

Why Share Certificates Can Help When Inflation Feels High

- You can lock in a rate for a set period, which can help if rates drop later

- You can use them for goals with a known timeline, where you do not need immediate access

Things to Watch Out For

- Early withdrawal penalties vary, so check the terms before you open a share certificate. [9]

- Auto-renewal and grace periods matter. Federal rules address notice requirements for certain automatically renewing time accounts and reference grace periods. [10]

12-Month Certificate at 3.70% APY‡ vs Inflation

Let’s say you put $10,000 into a 12-month certificate earning 3.70% APY‡ with interest compounded daily and credited monthly. Your balance at the end of the year would be $10,370.

Like the previous examples, let’s assume inflation runs at 3%. Therefore, you’d still need $10,300 to beat inflation.

- Change in purchasing power: $10,370 − $10,300 = $70

In this scenario, your certificate balance matures at $10,370, which puts you about $70 ahead of inflation in purchasing power at the end of the year.

Open a Sun East 6 or 12-Month Certificate and Earn!

If you know you won’t need immediate access to your cash, a Sun East Certificate can help you earn 3.70% APY‡ at the time of publication.

- Earn 3.70% APY‡

- Open your certificate with just $500

- No limits on your opening deposit

Learn more about Sun East Certificates.

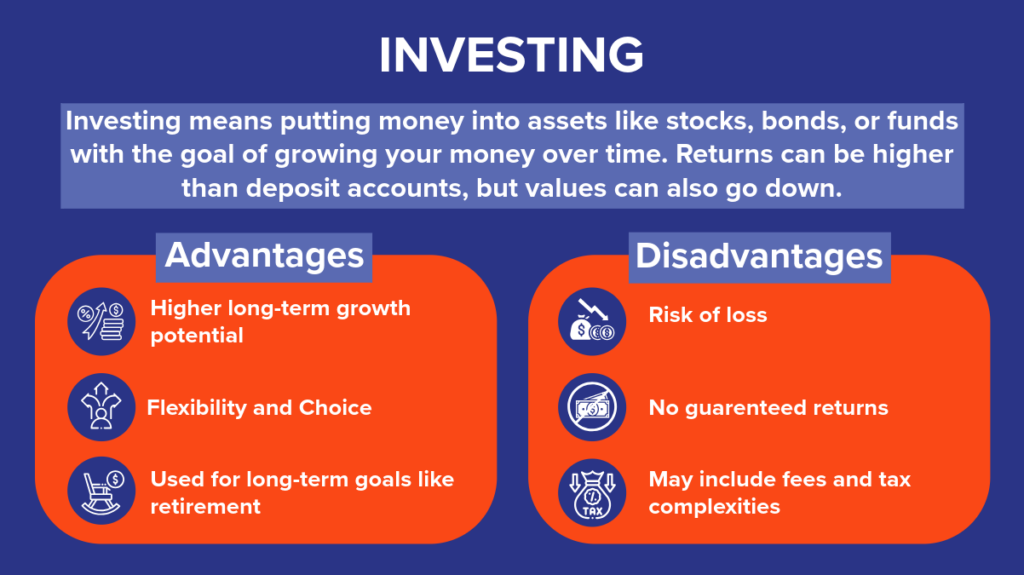

Investing for long-term inflation resistance

If your goal is years in the future, investing can play a role because inflation protection often requires long-term growth. Investing brings risk, including the possibility of loss, and investments are not federally insured like deposit accounts. [13]

This post does not give personal investment advice, but you can use a simple guideline:

- Short-term money: keep it safe and accessible.

- Long-term money: consider an investment strategy that matches your timeline and comfort level.

If you want guidance tailored to your situation, consider speaking with a qualified financial professional at Sun East Retirement and Investment Services.

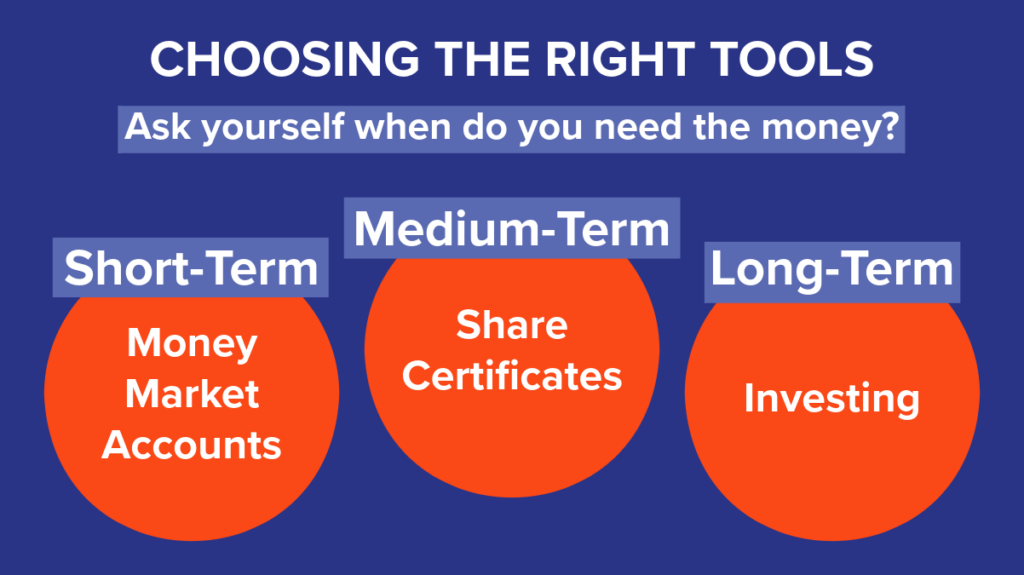

A simple guide to choosing the right mix

You do not need one perfect product. Many people use a mix based on what each dollar needs to do.

If you need the money soon

A Money Market Account can make sense because you can access funds while still earning interest. [6], [8]

If you can lock the money up for a set time

Share Certificates can work well, especially if you build a ladder to balance access and rate stability. [9], [11], [12]

If the goal is long-term

Consider whether investing fits your timeline and risk comfort. [13]

Set yourself up for success in 2026

Inflation can feel frustrating, but you have options. Start with your goal, pick a tool that matches your timeline, and focus on steady progress. Even one change can help you protect your buying power and build momentum in 2026.

This article shares general educational information and does not provide tax, legal, or investment advice.

+ APY = Annual Percentage Yield (APY) as of 12/22/2025. APY assumes that dividends are reinvested. Valid on new money only. New money defined as funds from another institution and not on deposit at Sun East within the prior 6 months. Failure to maintain minimum deposit could result in decreased earnings. Minimum daily balance to avoid imposition of Monthly Service Fee is $2,500. A Monthly Service Fee of $10 will be charged each monthly statement cycle if the daily balance falls below $2,500 during the monthly statement cycle.

‡ APY = Annual Percentage Yield (APY) as of 12/22/2025. APY assumes that dividends are reinvested. Withdrawal of dividends will reduce earnings. Earnings may be reduced if fees are incurred. Rates are subject to change without notice.

Sources

(1) SEC Investor.gov: What is Risk?

(2) BLS: Purchasing power and constant dollars

(3) Federal Reserve Bank of St. Louis: Adjusting for Inflation

(4) SEC Investor.gov: Risk and return

(5) SEC Investor.gov: Real Return

(6) CFPB / Regulation DD (Truth in Savings)

(7) FDIC: National Rates and Rate Caps

(8) CFPB: What is a money market account?

(9) CFPB: What is a certificate of deposit (CD)?

(11) FDIC: CD laddering example