When you need extra funds, the right borrowing option depends on what you need the money for, how much you need, and how you want to repay it. For homeowners, a Home Equity Line of Credit, or HELOC, can offer flexible access to funds by letting you borrow against the equity you have built in your home.

People use HELOCs for all kinds of expenses. Some use them for home improvements, repairs, or renovations. Others use them for debt consolidation, education costs, medical bills, emergency expenses, or other major life events, like weddings or travel. Because a HELOC works as a revolving line of credit, it can be especially helpful when costs happen over time instead of all at once.

Check out this article to learn more about how HELOCs work.

Still, a HELOC is not the right fit for every situation. Before you borrow against your home, it is important to understand how a HELOC compares to other options, like credit cards, Home Equity Loans, and personal loans. Here’s a closer look at how these products differ and when a HELOC may make sense for your needs.

HELOC vs Credit Card

While it’s similar to a credit card, a HELOC works differently in several key ways. Both are revolving forms of credit, which means you can borrow, repay, and then borrow again. But unlike a credit card, a HELOC is secured by your home’s equity.

That means a HELOC may come with a higher borrowing limit and a lower interest rate than a credit card, but it also carries more risk. If you fall behind on payments, your home could be at risk. Credit cards, on the other hand, are usually unsecured, but they often have higher interest rates and are typically better suited for smaller purchases or short-term borrowing.

One big difference is that HELOCs have a time limit.

- First, there’s the draw period. This is generally a 10-year period where you can withdraw and use the money in a HELOC. You’ll often still need to make payments during this phase and those payments will go toward interest.

- Second is the repayment period. Once you enter this period, you can no longer borrow from the line of credit and must begin repaying both principal and interest. The repayment period often lasts 10 to 20 years, though terms vary by lender. If you sell your home before the balance is fully repaid, the remaining amount will typically be due at closing.

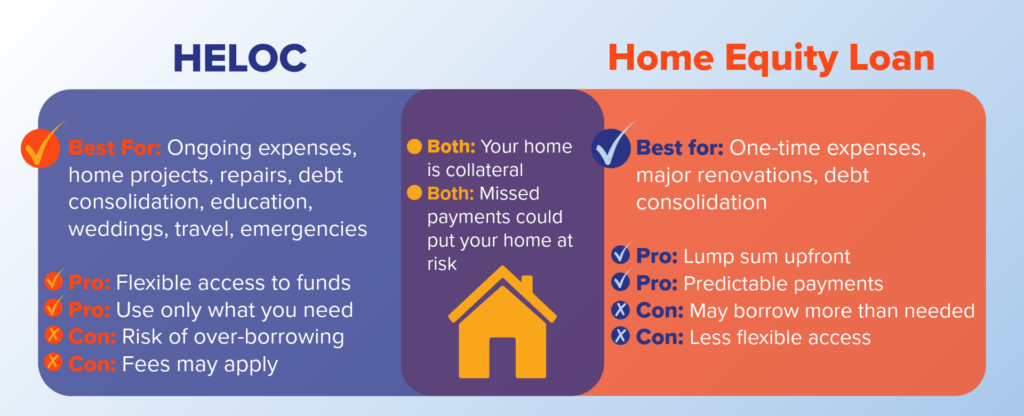

HELOC vs. Home Equity Loan

A HELOC and a Home Equity Loan both let you borrow against the equity in your home, but they work in different ways.

- A HELOC gives you a revolving line of credit that you can use as needed during the draw period. This can make it a strong fit when expenses happen over time or when you do not know the exact amount you will need right away.

- A Home Equity Loan gives you a lump sum up front and usually comes with a fixed interest rate and fixed monthly payment. This can make budgeting easier, especially when you know exactly how much you need to borrow.

Learn more about the differences between HELOCs and Home Equity Loans.

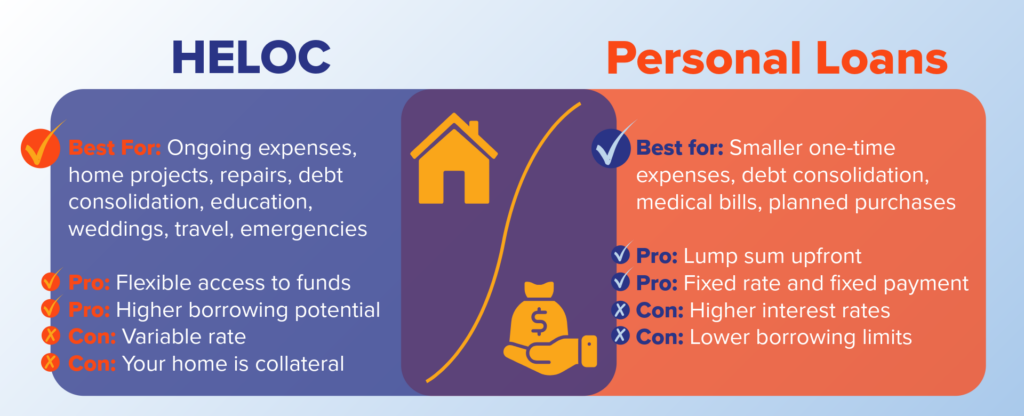

HELOC vs. Personal Loan

A personal loan can also be an alternative when you need extra funds. The biggest difference is that a HELOC is secured by your home, while most personal loans are unsecured.

Because a HELOC uses your home as collateral, it may offer a higher borrowing limit and a lower interest rate than a personal loan. That can make it appealing for larger expenses; however, that lower rate comes with added risk because your home is on the line.

A personal loan usually gives you a lump sum with a fixed rate and fixed repayment term. That structure can make it easier to budget and understand exactly what you owe each month.

HELOCs For Debt Consolidation

Using a HELOC for debt consolidation can help you combine multiple balances into one line of credit. This may be appealing if you are juggling high-interest debts like credit cards and want a simpler way to manage repayment.

One potential benefit of using a HELOC for debt consolidation is the chance to secure a lower interest rate than you would get with credit cards or some personal loans. A HELOC can also give you flexibility, since you may be able to draw only what you need to pay off your existing balances. If lowering your monthly payment is your main goal, a HELOC may help by spreading repayment over a longer period.

Still, there are important risks to consider. Unlike credit card debt, a HELOC is tied to your home. That means you are turning unsecured debt into debt backed by your property. If you fall behind on payments, you could put your home at risk. HELOCs also often come with variable rates, so your payment could rise over time. In some cases, that can make your debt harder to manage instead of easier.

Debt consolidation with a HELOC may make sense for borrowers who have strong equity, stable income, and a clear payoff plan. But if taking on debt against your home feels too risky, or if a variable rate does not fit your budget, another option may be a better fit, such as a consolidation loan.

To learn more about how a HELOC can help streamline debt payments, check out Kathleen’s story and how a HELOC helped her drastically reduce her monthly payment.

Is a HELOC Right For You?

So, is a HELOC right for you? The answer depends on your goals, your budget, and your comfort level with using your home as collateral.

A HELOC may make sense if you need flexible access to funds, expect expenses to happen over time, and want an option that may offer a lower rate than unsecured borrowing. It can be a strong fit for ongoing home projects, repairs, or even debt consolidation when you have a clear repayment plan in place.

On the other hand, a HELOC may not be the best choice if you need a one-time lump sum, want fixed monthly payments, or do not feel comfortable tying your borrowing to your home. In those cases, a Home Equity Loan, personal loan, or another financing option may fit better.

The best way to decide is to look closely at why you need the money, how much you need, and how you plan to pay it back. When you understand the tradeoffs, you can choose the borrowing option that fits your needs with more confidence.

[to add to “What is a HELOC?” Article when this is published]

Next Steps

Check out this article comparing HELOCs to other loan products like Home Equity Loans, Credit Cards, and Personal Loans, to explore whether or not a HELOC is the right choice for you.