Buying a car can feel like you are stuck in the passenger seat, especially once you step into a dealership. Many people assume the dealer’s financing offer is the only option; however, you have the power to take the wheel and shop around for better deals. [1], [2]

This blog walks you through the main automobile financing paths, discusses how to compare offers, and clues you in on what to watch for before you sign. So, without further ado, let’s hit the road!

Always Start With What You Can Afford

Before you look at cars or loans, pick a monthly payment that works for your budget and leaves breathing room for everything else in your life. The Consumer Financial Protection Bureau (CFPB) suggests you plan ahead for the full cost of borrowing and the overall vehicle cost, not only the monthly payment. [3], [4]

Sun East members get a free quote for exclusive discounts on auto insurance through our partner TruStage.* Find out how much you could save through TruStage Insurance or by calling the TruStage Call Center at 888.380.9287.

Know Your Financing Options

You have more than one path to financing. The Federal Trade Commission (FTC) and CFPB describe two primary routes: direct lending and dealer-arranged financing. [2], [5]

Option 1: Direct lending (for instance, credit union financing)

With direct lending, you apply for a loan directly through a lender before you shop for a vehicle. The FTC describes this approach as borrowing from a bank, finance company, or credit union and using that loan to buy the car from the dealer. [5]

Why people like it

- You can compare offers before you feel time pressure at the dealership. [6]

- You can walk in knowing what loan terms you qualify for, which helps you stay within budget. [6]

Sun East offers direct lending to members and can help you finance your next car. Visit our Vehicle Loans page to learn more about how we can get you on the road for as low as 5.24% APR+!

Option 2: Dealer-arranged financing

With dealer-arranged financing, the dealership helps you apply for a loan and matches you with a lender. CFPB explains that dealer-arranged financing often involves the dealer collecting your information and submitting it to lenders. [7]

Why people choose it

- It can feel convenient because you handle the car and financing in one place. [5]

What to watch for

- The loan terms still matter, even when the process feels simple. Compare the dealer’s offer with at least one outside offer so you can decide with confidence. [1], [3]

Option 3: Buy Here Pay Here financing

Some dealers offer in-house financing, often called Buy Here Pay Here. This option can carry higher costs and tighter terms, so you should review the details carefully and compare alternatives if you can.

Consumer.gov warns that dishonest dealers can use financing tactics that raise costs beyond what you expected. [8]

Compare Your Offers the Right Way

You will see plenty of ads and quotes that focus on one number, the monthly payment. A low monthly payment can hide a higher total cost if the loan term stretches longer, or the amount financed includes add-ons.

CFPB recommends you compare offers using multiple terms, not only the payment. [3]

What to compare besides the monthly payment

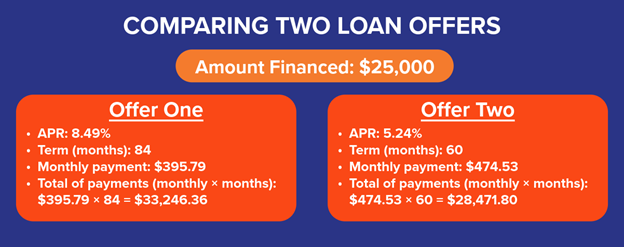

CFPB recommends looking at these details when you compare auto loan offers: [3]

- Amount financed

- APR

- Term (months)

- Monthly payment

- Total of payments over the life of the loan (monthly payment × months)

Despite a lower monthly payment, offer one costs more because the APR is higher and the loan term is longer. Offer two has a higher monthly payment, but costs less overall because the APR is lower, and the term length is shorter.

Sun East members are eligible for an additional 0.25%** discount on their loan payments when they use automatic payment transfer from a Sun East Checking Account. Learn more about the other benefits of a Sun East Auto Loan.

Use preapproval to reduce pressure

Preapproval can help you stay grounded while you shop. CFPB explains that preapproval can help you compare interest rates and stay within your budget before you reach the dealership. You still keep the option to use dealer financing if you get a better offer. [6]

Watch For Common Dealership Pitfalls

Most dealerships want to help you close a deal. Some tactics can make the deal more expensive than you intended. The FTC and Consumer.gov highlight risks like confusing paperwork, unexpected add-ons, and “yo-yo” financing problems. [8], [10], [11]

1) Keep the Deal Clear and Readable

Ask for a full breakdown of price and financing terms. Review the documents before you sign. Consumer.gov warns that some dealers try to change the cost of financing or add charges you did not expect. [8]

2) Treat Add-Ons Like Separate Decisions

Add-ons can raise the amount you finance, which raises your total cost over time. If you do not want an add-on, ask to remove it and confirm the final numbers before you sign. The FTC describes cases where dealers packed financing with add-ons without clear consumer consent. [12]

3) Understand “Yo-Yo” Financing Risk

A yo-yo financing problem can happen when a dealer lets you take the car home before the financing becomes final, then calls you back later to sign a new contract with worse terms. The FTC warns consumers about this practice and encourages comparison shopping and careful review of financing terms. [10]

If the dealer says the financing is not final, ask what that means in writing. If you feel uncomfortable, pause the deal and review your options.

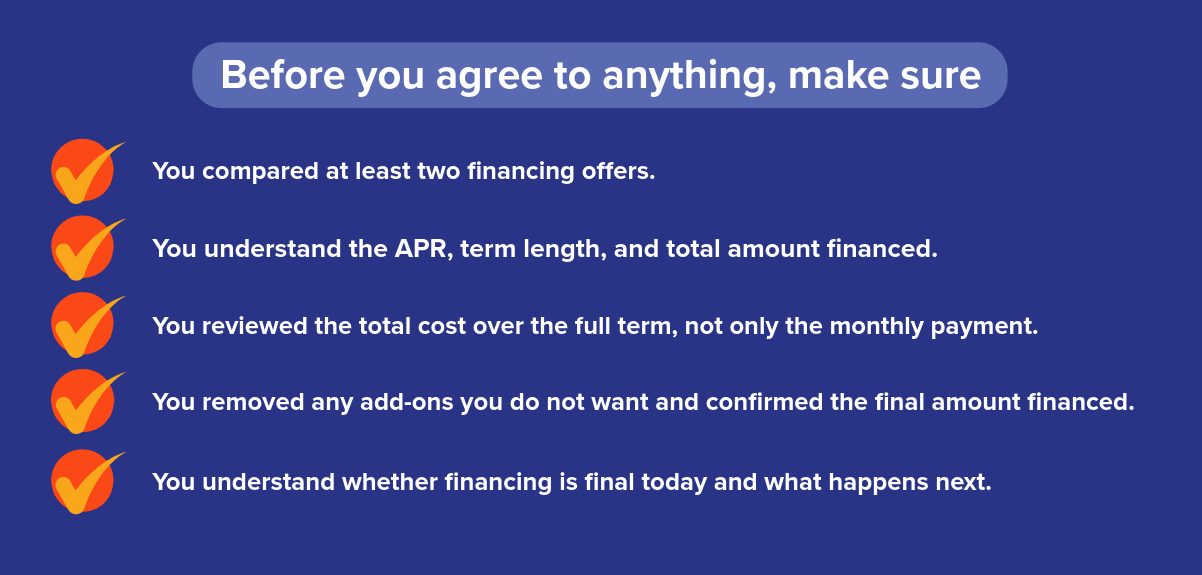

Pre-Signing Checklist!

Use this quick checklist right before you agree to anything:

You’re Ready to Hit the Road!

You do not need to become a car expert to make a smart decision. You just need time, a comparison plan, and the confidence to shop your options. When you compare financing offers and focus on total cost, you put yourself in control of the deal. [3], [6]

+ APR = Annual Percentage Rate; effective 01/20/2026 and subject to change without notice. APR includes 0.25% discount for Automatic Payment Transfer from Sun East checking. Loan rates are determined by member’s creditworthiness as well as other factors including term of the loan, line requested and loan-to-value ratio. Top tier rates listed are available to highly credit-qualified individuals.

*TruStage™ Auto and Home Insurance program is offered by TruStage™ Financial Group, Inc. and issued by leading insurance companies. Discounts are not available in all states and discounts vary by state. The insurance offered is not a deposit and is not federally insured. This coverage is not sold or guaranteed by your credit union.

** 0.25% discount for Automatic Payment Transfer from Sun East checking. If at any time, Automatic Payment Transfer is discontinued then rate discount will be discontinued.

Third party linked websites are not under the control of Sun East Federal Credit Union. We are not responsible for their content. Third party website privacy and security policies may differ from ours. If you choose to engage in a transaction with a third party, please note that we do not represent either you or the third party in that transaction.

Sources

(1) CFPB: Am I required to get my auto loan through a dealership?

(2) CFPB: What are the different ways to buy or finance a car or vehicle?

(3) CFPB: How do I compare auto loan offers? What should I look at besides the monthly payment?

(4) CFPB: What should I know before I shop for a car or auto loan?

(5) FTC Consumer Advice: Financing or Leasing a Car

(6) CFPB: Shopping for your auto loan

(7) CFPB Newsroom: Know you owe auto loans shopping sheet

(8) Consumer.gov: Getting a Car Loan

(9) CFPB: Take control of your auto loan guide

(10) FTC: Avoiding a Yo-Yo Financing Scam

(11) CFPB: Take control of your auto loan

(12) FTC Business Guidance Blog: Deal or no deal? FTC challenges yo-yo financing tactics