Credit cards and personal loan debt feel heavy because they restrict your choices and limit your financial freedom. However, the good news is you can make real progress paying down your debts in 2026 by creating and sticking to a clear, actionable plan.

This guide walks through a five-step plan to help you pay off your debts, giving you the tools to stay consistent and avoid common debt scams.

- Step 1: Get Clear on What You Owe

- Step 2: Choose a Payoff Strategy You Can Stick To

- Step 3: Build a Plan That Survives Real Life

- Step 4: Find Extra Money Without Burning Out

- Step 5: Use Tools That Can Speed Things Up and Avoid Common Traps

Let’s jump in!

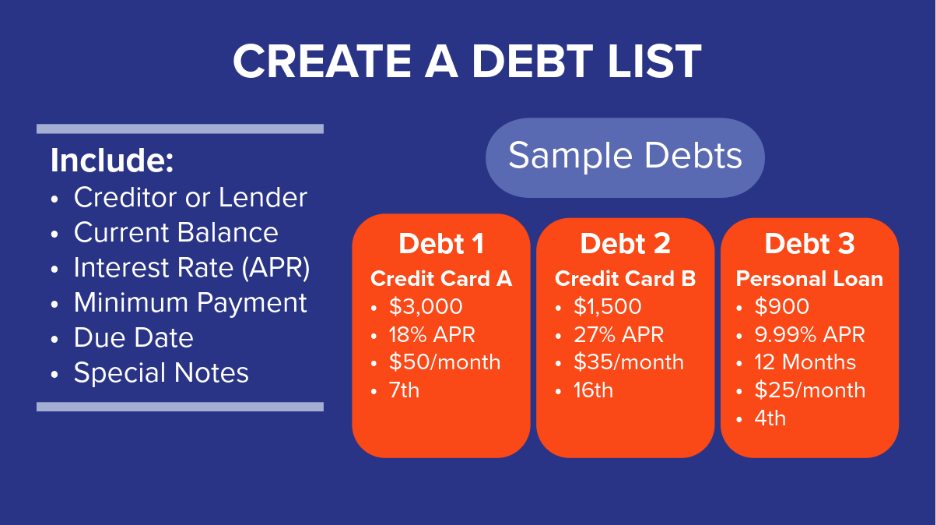

Step 1: Get Clear on What You Owe

Before you pick a strategy, build a simple debt list laying out all your debts. This gives you clarity, helps you see the big picture, and keeps you from missing payments.

Step 2: Choose a Payoff Strategy You Can Stick To

The Consumer Financial Protection Bureau (CFPB) highlights two common debt payoff strategies:

- Avalanche Method

- Snowball Method

Both assume that you pay the monthly minimums on all your debts. The big difference is what debt you target with extra money beyond those minimum payments. [1], [2]

Let’s learn more about each option so you can pick the strategy that fits your situation best.

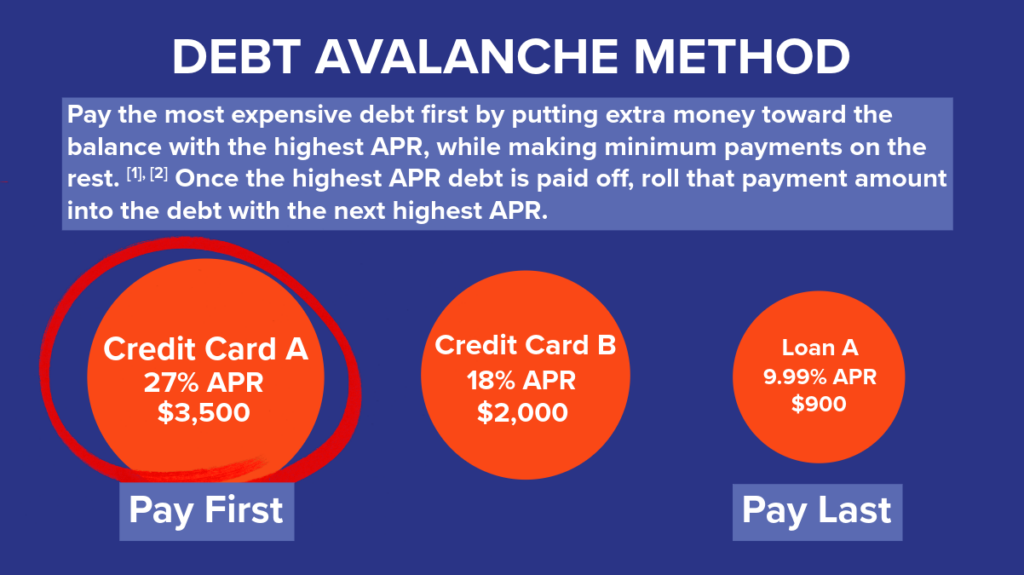

The Debt Avalanche Method generally reduces the amount of interest you pay over time because you’re prioritizing paying the most expensive debt. In many cases, this is the method you should choose if you want to pay the least amount of interest.

The Debt Snowball Method is designed to create quick progress by clearing small balances first. CFPB points out the motivation upside while noting that you may pay more overall because you might not eliminate the costliest debt first.

However, if you have many debts with comparable interest rates, this option will help you eliminate your smaller debts first.

If you feel stuck, pick the method that matches your biggest challenge:

- You wan to pay less interest overall: Choose avalanche. [2]

- You want quick wins to stay motivated: Choose snowball. [2]

Either way, follow one rule every month: pay the minimum on every debt, then send your extra payment to one focus debt. [1]

Step 3: Build a Plan That Survives Real Life

A plan only works if it fits your real month, not your ideal month.

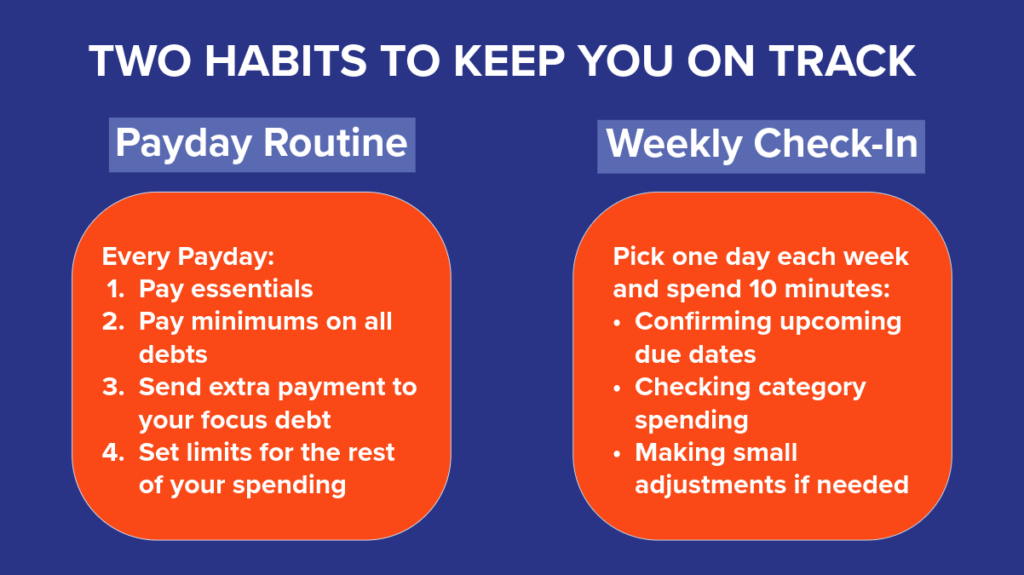

Pay your essentials first so you do not create new problems while you work on debt. [10], [11] Check out our blog post on budgeting to learn how to build an effective budget.

After you cover the essentials, pay your debt minimums and apply any extra money to your focus debt. [12]

A small buffer helps you avoid adding new debt when life throws a surprise at you. [13] Start small and keep it simple:

- Aim for a starter buffer you can build in a few paychecks.

- Keep it separate from spending money.

- Refill it after you use it.

The key is to build easy-to-follow habits that you can stick with while you pay down your debts. [14]

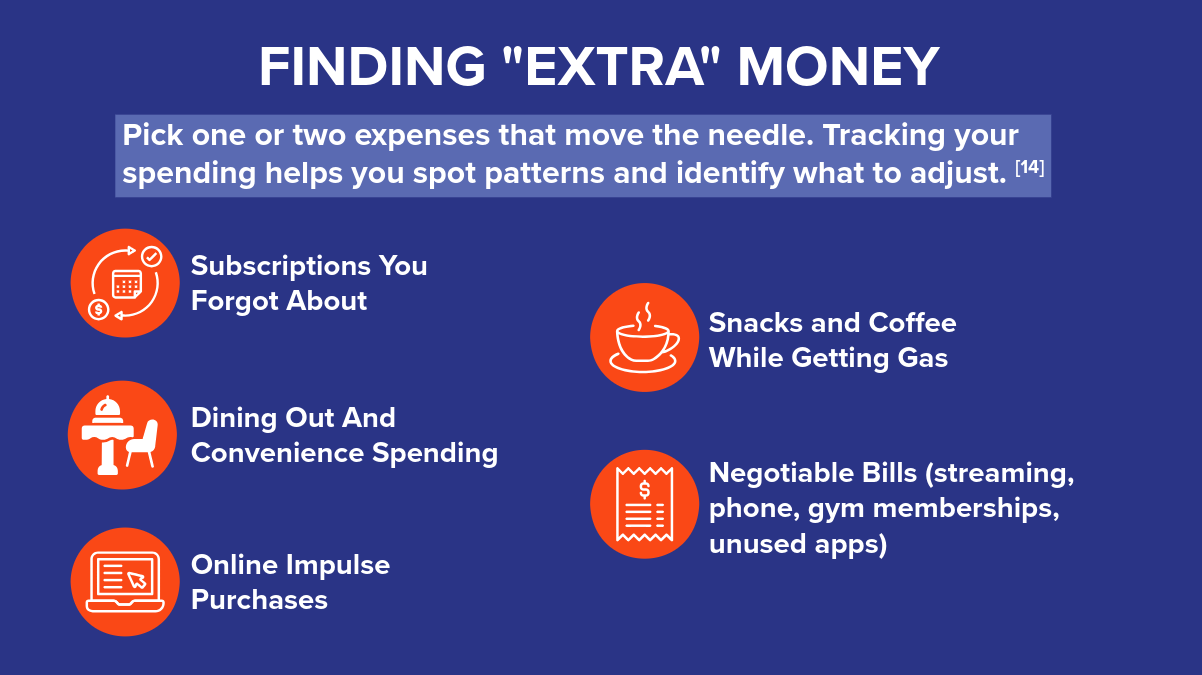

Step 4: Find Extra Money Without Burning Out

Debt payoff rarely comes from one big change in your budget. It usually comes from a few small changes you can consistently repeat. [14]

When you receive extra money like a bonus, tax refund, or cash gift, decide ahead of time how you will use it. [14]

- Put a set percentage toward your focus debt.

- Use the rest for essentials, a buffer, or planned expenses.

Step 5: Use Tools That Can Speed Things Up and Avoid Common Traps

Some tools can help you pay debt faster. They also come with tradeoffs. Read terms carefully and make sure the math works for your situation.

Balance transfers for credit card debt

A balance transfer lets you move a balance from one credit card to another, sometimes for a fee. [3] Credit card companies may offer promotional rates for a limited time. [3]

What to watch for

- Balance transfer fees: A card issuer can charge a balance transfer fee, even on a 0% offer. [4]

- Promo rate timing: An introductory rate generally must last at least six months unless you are more than 60 days late on a payment. [5]

- New spending: A balance transfer works best when you stop adding new card debt.

A balance transfer can help when you can pay the balance down before the promotional period ends, and the fee still makes sense.

A Sun East Platinum Mastercard® has no balance transfer fees + and a 0% introductory rate for the first 6 months. Learn more about our credit card offerings.

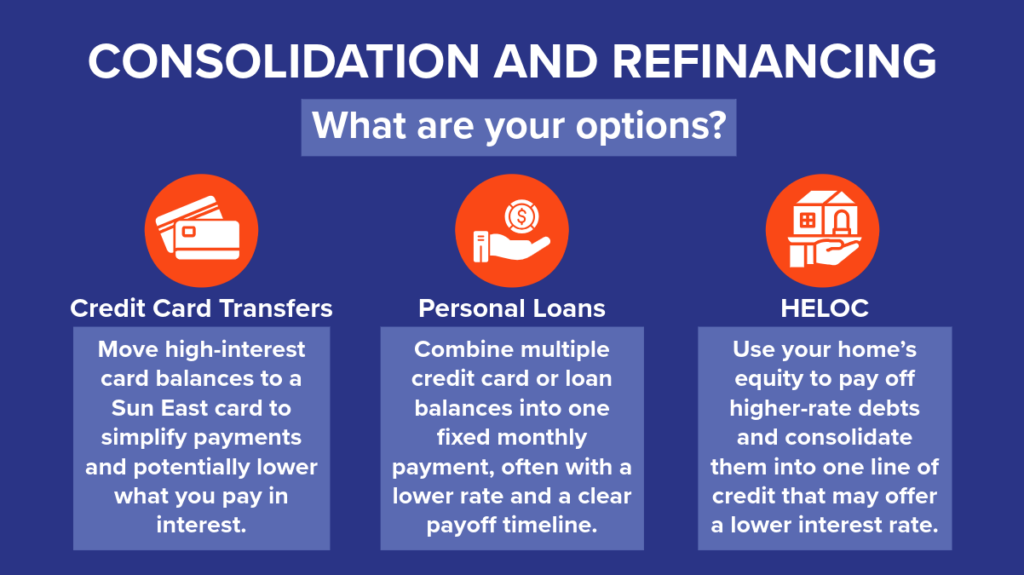

Consolidation and Refinancing

You have two options that may help you organize your debts, lower your monthly payments, or lock in a lower rate.

- Consolidation combines multiple debts into one payment.

- Refinancing replaces a loan with a new loan, ideally at a lower rate.

Sun East offers three ways you can refinance or consolidate your credit card and personal loan debts.

Learn more about Sun East Personal Loans and HELOC options.

These tools can help reduce your rate, simplify your payments, or give you a clearer payoff timeline. Compare the total cost, not just the monthly payment.

Learn more about debt consolidation options at Sun East.

Student loans deserve their own decision path

Federal student loans are in a special class of debt because they come with repayment options like income-driven repayment plans (IDR plans) that do not apply to most private loans. [6], [7]

Avoid debt relief scams

Scammers often target people who feel stressed about credit card debt and student loan debt. The Federal Trade Commission (FTC) warns about common red flags.

Key scam warnings

- Do not pay upfront fees for debt relief services. The FTC warns that charging upfront fees for certain debt relief help is illegal. [8], [9]

- Be cautious with anyone who guarantees results or pressures you to act fast. The FTC flags these claims as common scam tactics. [8], [9]

- Do not share sensitive personal information with unexpected callers who promise easy fixes. The FTC highlights this risk in scam guidance. [8]

If you feel unsure, slow down and verify the company and the offer.

Wrap-up: Your 2026 payoff mindset

You do not need a perfect plan. You need a plan you can repeat. If one month goes off track, restart with your next paycheck. Consistency builds momentum, and momentum brings you closer to freedom from your debt!

This article shares general educational information and does not provide tax, legal, or investment advice.

+ Balance transfer fees waived on balance transfers.

Sources

(1) CFPB: How to reduce your debt

(2) CFPB: Reducing debt worksheet

(3) CFPB: Credit cards key terms

(4) CFPB: What is a balance transfer fee?

(5) CFPB: How long can I keep a low rate on a balance transfer or other introductory rate?

(6) Federal Student Aid: Income-Driven Repayment (IDR) Plan

(7) Federal Student Aid: Top FAQs about Income-Driven Repayment Plans

(8) FTC: Carrying credit card debt? How to avoid debt relief scams

(9) FTC: Paying for school and avoiding scams

(11) CFPB: Behind on bills? Start with one step.

(12) CFPB: Debt action plan tool